Australian Federal Budget 2026-27

On Tuesday, 12 May 2026, Treasurer Jim Chalmers handed down the 2026-27 Federal Budget, his 5th Budget.

This budget includes some of the most significant proposed tax reforms in recent years.

Many of the proposed measures target capital gains tax, investment properties and discretionary trusts, and may significantly impact investment and business structures going forward.

Please note that many of these measures are currently proposals only and will still require legislation to become law.

Below is a summary of the key proposed measures.

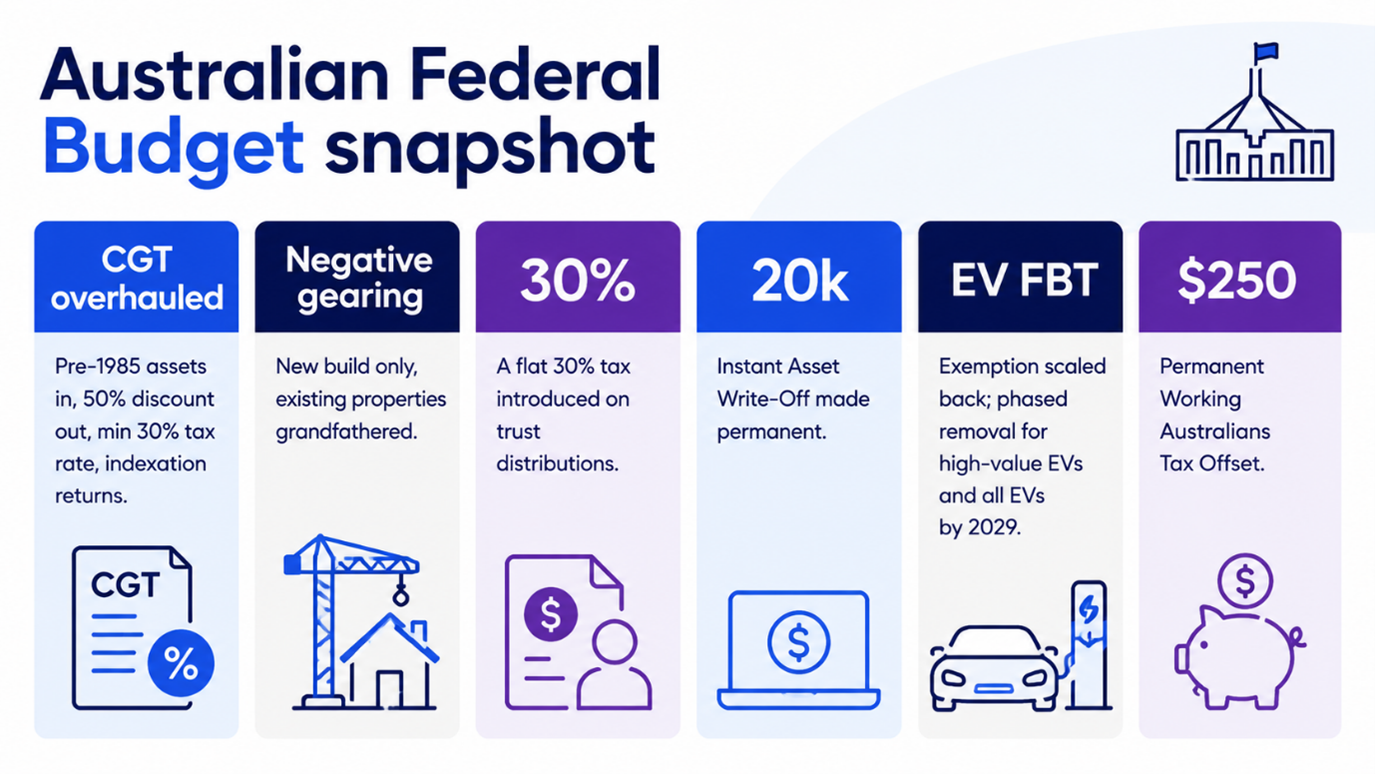

1.Capital Gains Tax (‘CGT’) Changes – Proposed from 1 July 2027

The Government has proposed replacing the current 50% CGT discount with an inflation-based indexation method for assets held longer than 12 months.

Under the proposal:

· Capital gains accrued before 1 July 2027 would still receive the current 50% CGT discount

· Gains accruing after 1 July 2027 would instead use an indexed cost base method

· A proposed minimum effective 30% tax rate on net capital gains would also apply

Importantly, assets acquired before 20 September 1985 (“pre-CGT assets”) are also proposed to come into the CGT system from 1 July 2027 for future gains.

This means:

· Existing unrealised gains up to 30 June 2027 are proposed to remain exempt under current rules

· Future gains after 1 July 2027 may become taxable

The Government has indicated transitional rules would apply to existing investments.

There is currently an exception proposed for new residential properties where investors may choose between:

· the current 50% CGT discount; or

· the new indexed cost base method

2.Negative Gearing – Proposed Changes from 1 July 2027

The Government has proposed restricting negative gearing on residential investment properties to new residential builds only.

Under the proposal:

· Existing residential investment properties owned before Budget night (7:30pm AEST, 12 May 2026) would be grandfathered and continue under current rules until sold

· Contracts entered into before Budget night but settling later are also proposed to be grandfathered

· Established residential properties acquired after Budget night may have restrictions on using rental losses against salary and wage income from 1 July 2027

For affected properties:

· Rental losses would only be able to offset future rental income or capital gains from residential property

· Excess losses would be carried forward rather than offset against salary and wage income

New builds are proposed to remain eligible for negative gearing concessions.

3.Discretionary Trust Changes – Proposed from 1 July 2028

The Government has proposed introducing a minimum 30% tax on discretionary trust income from 1 July 2028.

Under the proposal:

· Trustees would pay a minimum 30% tax on trust taxable income

· Beneficiaries other than corporate beneficiaries would generally receive non-refundable credits for the tax paid

· Corporate beneficiaries will be assessed based on the trust income to which they are entitled, without being able to claim credits for tax payable by the trustee.

This may reduce the effectiveness of distributing trust income to low-income beneficiaries

The proposed rules are not expected to apply to Fixed trusts, Superannuation funds, Deceased estates, Charitable trusts, and Certain primary production income.

The Government also announced proposed rollover relief for three years from 1 July 2027 to assist restructuring from discretionary trusts into companies or fixed trusts.

4.Business Measures

Permanent $20,000 Instant Asset Write-Off

The Government has proposed making the $20,000 instant asset write-off permanent from 1 July 2026 for eligible small businesses with turnover under $10 million.

Loss Carry-Back Rules

From 1 July 2026, companies with turnover under $1 billion may again be able to carry tax losses back up to two years to offset prior year tax paid.

Refundable Tax Offset for Start-Up Companies

From 1 July 2028, eligible start-up companies with turnover under $10 million that generate tax losses during their first two years of operation may be able to access a refundable tax offset.

The refundable offset is proposed to be limited to the amount of:

· PAYG withholding; and

· Fringe Benefits Tax (‘FBT’)

paid in relation to Australian employees.

This measure is aimed at assisting start-up businesses during their early growth phase when businesses are often operating at a loss.

Electric Vehicle (‘EV’) FBT Changes

The current FBT exemption for electric vehicles is proposed to gradually phase out.

Under the proposal:

· Existing novated lease arrangements are expected to be grandfathered

· New novated leases for eligible EVs under $75,000 may continue to access the current FBT exemption until 1 April 2029

· From 1 April 2029, the full exemption is proposed to end and instead a concessional FBT treatment equivalent to approximately a 25% reduction may apply

Clients considering entering into EV novated lease arrangements may wish to review timing prior to the proposed changes taking effect.

Research and Development (‘R&D’) Tax Incentives

From 1 July 2028, the Government has proposed changes to the R&D tax incentive regime aimed at simplifying the rules and increasing support for eligible businesses undertaking genuine R&D activities.

Key proposed changes include:

· Increased R&D tax incentive rates for eligible core R&D activities

· Increased turnover threshold from $20 million to $50 million for access to refundable offsets

· Increase in maximum eligible R&D expenditure threshold from $150 million to $200 million

· Tighter rules around smaller and supporting R&D claims

Businesses currently claiming or considering R&D tax incentives should review how the proposed changes may impact future eligibility and claim outcomes.

Dynamic PAYG instalment calculations

From 1 July 2027, small and medium businesses will be able to opt in to reporting and paying PAYG instalments monthly and to using an ATO-approved calculation embedded in accounting software to calculate and vary their instalments.

Taxpayers with a demonstrated history of non-compliance will be required to report and pay PAYG instalments monthly.

5.Individual Tax Measures

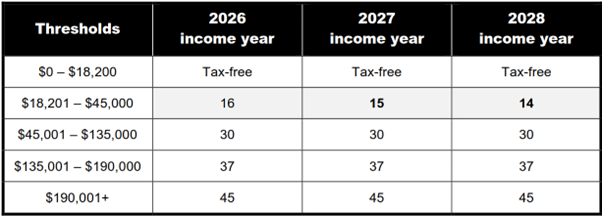

Tax Cuts Already Legislated

The previously legislated reduction in the individual tax rate for incomes between $18,201 and $45,000 remains unchanged:

• 15% from 1 July 2026

• 14% from 1 July 2027

$250 Working Australians Tax Offset

A proposed permanent $250 tax offset would apply from 1 July 2027 for salary and wage earners and sole traders.

$1,000 Standard Deduction

A proposed standard deduction of up to $1,000 for work-related expenses is expected to apply from 1 July 2026.

Eligible taxpayers may choose to claim the standard deduction without retaining receipts for work-related expenses up to $1,000. Taxpayers with higher deductible expenses may still claim actual expenses under the existing substantiation rules.

The standard deduction would apply in addition to other deductions such as charitable donations, union fees and professional membership subscriptions.

Medicare Levy Thresholds

Low-income Medicare levy thresholds are also proposed to increase from 1 July 2026.

· The threshold for singles will be increased from $27,222 to $28,011.

· The family threshold will be increased from $45,907 to $47,238.

· For single seniors and pensioners, the threshold will be increased from $43,020 to $44,268.

· The family threshold for seniors and pensioners will be increased from $59,886 to $61,623.

For each dependent child or student, the family income thresholds will increase by a further $4,338, up from the previous amount of $4,216.

Private Health Insurance (PHI) Rebate

The Government will remove the age-based uplift of the PHI Rebate from 1 April 2027.

Currently, individuals aged 65 and above are entitled to a higher rebate percentage.

Other Measures

Extending the ban on foreign purchases of established dwellings

The Government will extend the temporary ban on foreign purchases of established residential dwellings until 30 June 2029.

Our office will continue reviewing the Budget announcements and further details as legislation and guidance become available.

If you would like to discuss how these proposed changes may affect your circumstances, please feel free to contact our office.